Updated June 2026

What Is Collision Coverage Insurance?

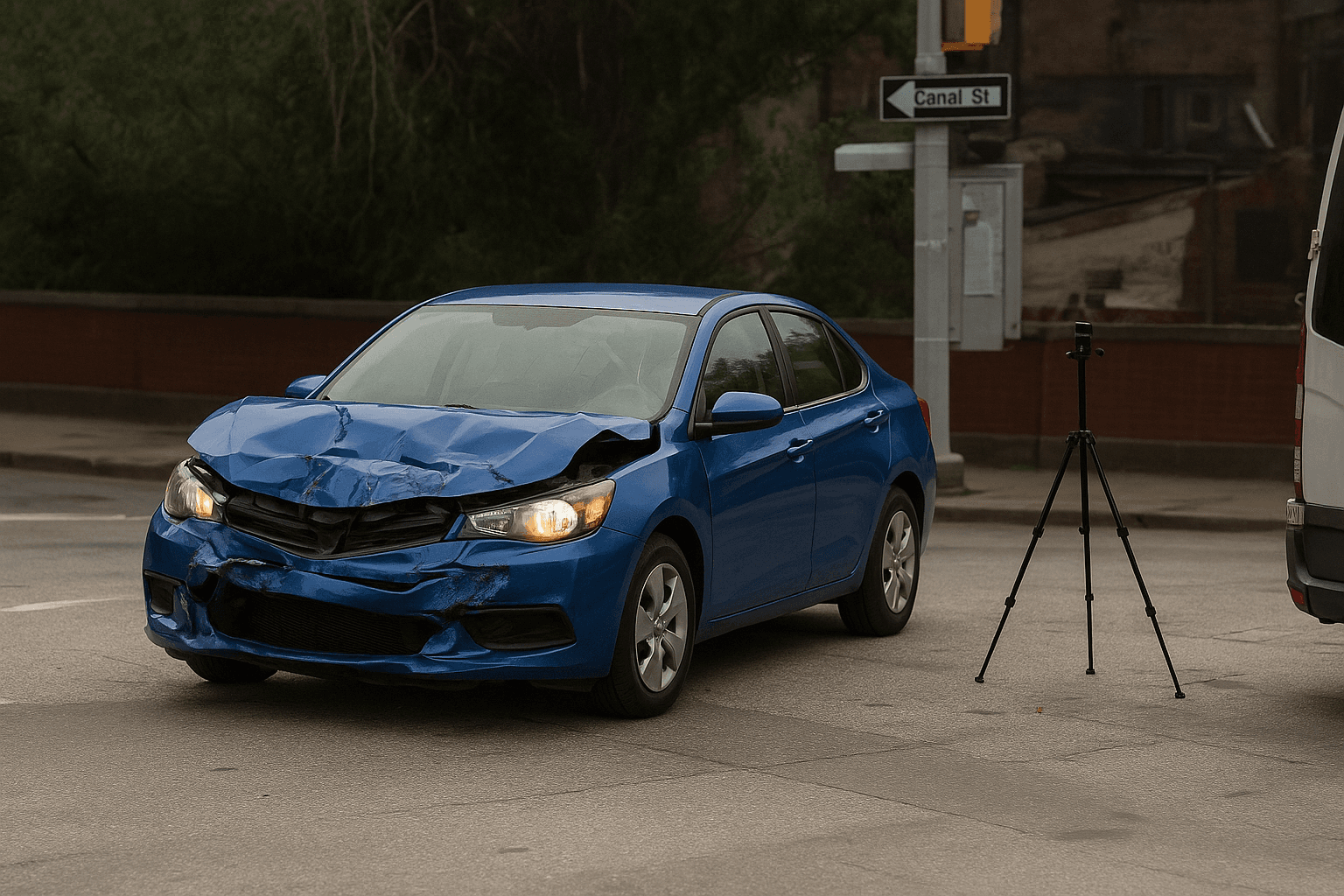

Collision coverage pays to repair or replace your vehicle after you collide with another car, a stationary object like a guardrail or tree, or when your car rolls over. Unlike liability insurance, which pays for damage you cause to others, collision covers your own vehicle regardless of who caused the accident. The claim pays up to your vehicle's actual cash value minus your chosen deductible, typically $250 to $1,000. Illinois does not require collision coverage by law, but your lender will mandate it if you're still making payments or leasing.

- You slide on black ice and hit a concrete barrier. Repairs cost $4,200. With a $500 deductible, collision pays $3,700. Your liability coverage pays nothing because you didn't damage another person's property. Without collision, you pay the full $4,200 out of pocket.

- You misjudge stopping distance and rear-end the car ahead at a red light. Your car has $2,800 in front-end damage; the other driver's car has $3,500 in rear damage. Your collision coverage pays to fix your vehicle minus your deductible. Your liability coverage pays for the other driver's repairs and any injury claims, up to your policy limits.

- Your 2012 sedan worth $3,200 is totaled after you hit a deer that darted into traffic. Collision pays the $3,200 actual cash value minus your $500 deductible — a $2,700 check. If your annual collision premium is $320, you've paid nearly ten percent of the vehicle's value each year for coverage that delivers $2,700 once.

Who Needs Collision Coverage Insurance?

Collision coverage makes sense if you're still paying off a car loan or lease — your lender requires it. It's also worth keeping if your vehicle is worth more than ten times your annual collision premium and you lack savings to replace it after an at-fault accident. Retirees who drive frequently in dense traffic, winter weather, or unfamiliar areas face higher accident risk and benefit from the coverage.

Multiply your annual collision premium by three. If that total exceeds your vehicle's current value, the coverage costs more than it's likely to pay out over the next few years. Add your deductible to the three-year premium — if the sum approaches or exceeds replacement cost, drop collision and bank the premium instead. Revisit this calculation annually as your vehicle depreciates.

How Much Does Collision Coverage Insurance Cost?

Collision adds $25 to $75 per month to a policy in Illinois, or roughly $300 to $900 annually, depending on vehicle value, your deductible, driving record, and location.

- Vehicle age and value — newer or higher-value cars cost more to insure because the maximum claim amount is higher.

- Deductible choice — a $1,000 deductible can cut your premium by 30 to 40 percent compared to a $250 deductible, but you pay more out of pocket per claim.

- Driving record — recent at-fault accidents or moving violations raise collision premiums because insurers price you as more likely to file a claim.

- Garaging ZIP code — urban Cook County ZIP codes often see premiums 20 to 50 percent higher than downstate Illinois due to accident frequency and repair costs.

- Annual mileage — retirees driving under 7,500 miles per year qualify for low-mileage discounts with most Illinois carriers, lowering collision costs by 10 to 20 percent.

- Credit-based insurance score — Illinois allows insurers to use credit history; a strong score can reduce collision premiums by 15 percent or more.